Investor Update - May 2022

- Marcus Bogdan

- Jun 8, 2022

- 2 min read

“There is currently extreme volatility across commodity markets, driven by a combination of global energy supply and security concerns, exacerbated by the impact of the Russian invasion of Ukraine, with subsequent unprecedented increases in international energy prices.”

Frank Calabria (CEO)

Origin Energy

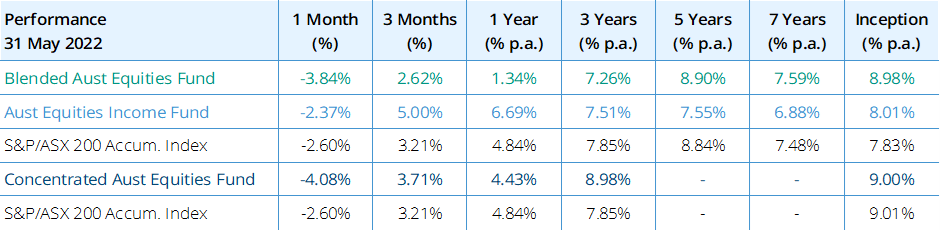

Higher volatility characterised the month of May, with the ASX 200 down 2.6%. A concerted push by central banks to tighten financial conditions to counter the chilling effects of inflation continued to weigh on equities.

The prospect of rising interest rates was particularly damaging to the Real Estate and Technology sectors which fell 8.9% and 8.7% respectively. Materials +0.1% was the only sector to manage a positive return for month.

Commodities were a welcome source of diversification in the portfolio as markets grappled with tightening financial conditions and persistent high inflation. BHP Group (BHP) and Santos (STO) provided an important ballast to the portfolios in a turbulent month. A prolonged period of under investment coupled with ongoing challenge of supply chain disruption as economies reopened has contributed to the sharp rise in commodity prices.

With a backdrop of rising raw material prices, the portfolios also benefited from exposure to Amcor (AMC) and Brambles (BXB) that had contractual pass-through price mechanisms to absorb higher costs.

Nevertheless, the portfolios were buffeted by Goodman (GMG), Macquarie (MQG), News Corp (NWS) and Woolworths (WOW) that were impacted by concern of higher interest rates and weaker than expected earnings results from the US bell weather stocks of Amazon, Target, and Walmart.

The healthcare sector recovery in volumes lost during the pandemic continues to face headwinds in Australia, as the impact of Covid/flu has resulted in delays in medical testing and elective surgery. Whilst the delayed backlog for patient care is inevitably weighing on health companies’ results in the short term, the recovery in earnings should be underpinned by the demand for the treatment for chronic disease, catch-up referrals, and an ageing population. Encouragingly, in the US CSL and key industry participants have highlighted that plasma collection volumes (depressed during Covid) are now returning to pre-Covid volumes.

We are seeing the first tangible signs that rising interest rates and high input costs are dampening both earnings momentum (with earnings revisions turning negative) and house prices declining for the first time in the cycle. Amid an economic environment characterised by slowing growth our clear preference is to be invested in companies that offer exposure to consumer staples and defensive industrial sectors. Moreover, in a period of high inflation we continue to hold commodity stocks that are benefiting from elevated prices and offer a hedge against inflation.

Comments