Investor Update - June 2025

- Marcus Bogdan

- Jul 17, 2025

- 5 min read

The ASX 200 June and 2025 financial year market Review

The ASX rose +1.4% in June, as equity markets continued to rebound from the April lows. Equity markets finished the financial year emboldened despite the profusion of uncertainties relating to geo-political tensions, a slowing global economy, and elevated valuations. The rally in equity prices has been driven by a continued expansion in valuation multiples. The ASX 200 trades on a 12-month forward PE ratio of ~18.9 times, which is within the top 90% of PE ratios in the last 40 years. The PE range for the ASX 200 over the last 40 years spans from a peak PE multiple of ~20.5 times (Yr 2000 Tech boom) to 8 times (Yr 2008 GFC), with a long-term average of 14.6 times.

Remarkedly, over the last two years valuation multiples have expanded while earnings per share have declined by around 9%, largely driven by a decline in commodity prices.

The strong performance in the ASX 200 over 2025 financial year masked a large dispersion in returns across industry sectors, with financial, technology, and telecommunication delivering stellar gains, while energy, healthcare and resource stocks were noticeably weaker.

Notably most of the gains in FY25 were driven by PE expansion and momentum in a concentrated number of stocks, with Commonwealth Bank (CBA) being the largest single stock contributor adding ~4.57% to the ASX 200 return.

For June at a sector level Energy (+9%) added the most value boosted by a recovery in the oil price and bid for Santos. Financials were the second-best performer underpinned by another strong contribution from CBA. The largest detraction for the market was in Resources, weighed down by a sharp sell-off in gold securities and weakness in the iron ore price.

Investment Observations

1. Adapting with Discipline in a Momentum-Driven Market

Our investment framework has long emphasised the investment fundamentals of: the quality of a company’s earnings, industry dynamics and competitive positioning, balance sheet resilience, and the alignment and execution of management teams. Historically, these metrics have proven to be reliable indicators of share price performance.

However, over the past two years, we have observed a significant shift in what drives shareholder returns. Share price momentum—fuelled by structural changes in how capital flows into equity markets—has become equally, if not more, important than fundamentals.

In light of this, we’ve taken the opportunity to reflect on what continues to serve us well, what we’ve learnt through recent market behaviour, and how we’ve refined the portfolio — all while remaining anchored to our long-term investment philosophy.

2. What We Know, what We’ve Learnt, and What We’ve Changed

What we know

Fundamentals remain the most enduring driver of long-term returns. We continue to believe:

• Earnings quality underpins resilience and long-term growth across market cycles.

• Valuation discipline is essential — long-term value is created by purchasing quality companies at reasonable prices.

• Diversification, thoughtfully applied, is both a source of return and a safeguard against uncertainty. In a market increasingly driven by flows and sentiment, maintaining a well-diversified portfolio improves the probability of capturing upside while managing downside risk

What we have learnt

Greater balance across sector exposures is essential. While we’ve traditionally emphasised differentiated sector positioning (e.g. underweight financials, overweight healthcare), recent experience has reinforced the importance of identifying exceptional companies within each sector.

This approach remains firmly aligned with our long-term investment philosophy: to invest in high-quality, resilient businesses with attractive return potential — wherever they sit within the index. In doing so, we enhance the robustness of the portfolio without compromising on conviction

What we have changed

We have adjusted the portfolio to ensure more balanced sector weightings while maintaining our quality bias:

• Increased exposure to financials primarily through diversified financials (Insurance), where valuations are more moderate and industry trends supportive.

• Rotated within healthcare toward names offering nearer-term value catalysts, including the addition of Sigma (Chemist Warehouse).

• Reduced cash weighting.

3. The Rise of Momentum: Passive Flows Reshape Market Leadership

Two major forces underpin this shift:

• Exchange Traded Funds (ETFs) and

• Industry Superannuation Funds.

ETF index buying and the weight of consistent superannuation contributions have led to disproportionate inflows into a narrow set of stocks. This flow-driven concentration is materially shaping the return profiles of listed equities.

4. Shrinking ASX and the Effects of De-Equitisation

Compounding this trend is the shrinking investable universe:

• The number of listed companies on the ASX is at a 15-year low.

• Over the past year, 7.6% of companies have delisted.

• Today, just five companies account for one-third of the ASX's total market capitalisation.

This process of de-equitisation, combined with the continual flow of funds into superannuation and ETFs, is inflating valuations. We are seeing the direct effect of this now as stock prices in Australia are pushing valuations to record levels without the support of solid earnings growth.

Figure 1: Number of stocks listed on the ASX

5. Capital Management: Shrinking Supply Meets Rising Demand

Adding further fuel to the fire, capital management trends are tightening share supply:

• Shareholders are favouring off-market buybacks over M&A or capital expenditure.

• The result is a reduction in outstanding shares at a time when demand remains structurally strong.

The interaction between rising demand and declining supply is pushing valuations to historic highs—even in the absence of robust earnings growth.

Figure 2: Rising EPS not required for rising prices

6. The CBA Phenomenon: A Case Study in Flow-Driven Valuation

The clearest example is Commonwealth Bank (CBA):

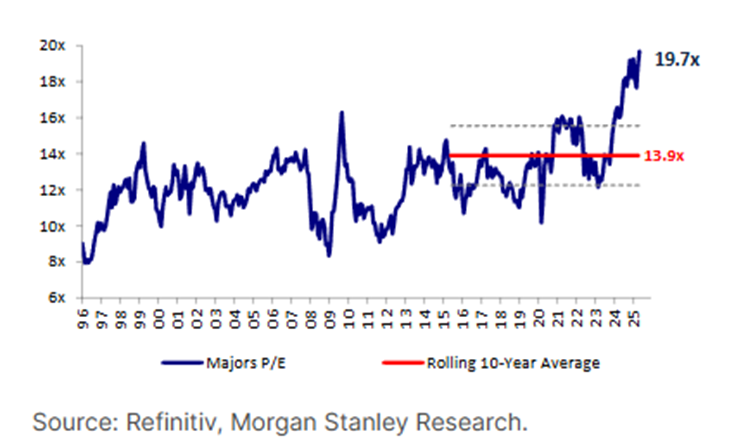

• CBA currently trades on a 12-month forward P/E of ~28x, double its long-term average of ~14x.

• It commands an ~80% premium to other major retail banks.

While we wholeheartedly acknowledge CBA’s strong excellent track record, CBA is clearly a beneficiary of the gravitational force of ETF and Industry Superannuation ‘flow of funds’ effect, whereby momentum trumps valuation.

A similar trend is visible in the ASX-listed technology sector, now trading at a record P/E of ~87x.

Figure 3: Major Banks: One-year Forward P/E Multiple.

Figure 4: CBA one-year Forward P/E Premium / (Discount) vs. Peer Average

Figure 5: Trading Range: One-year Forward P/E Multiple

Figure 6: Australian Healthcare P/E multiples - current vs 10-year average

Figure 7: CSL Valuation; Source: Factset

7. The Investor Dilemma: Momentum vs Valuation

Valuations that remain elevated at/or near record highs for an extended period pose an invidious challenge for investors.

• Does the investor suspend traditional valuation disciplines to follow momentum?

• Hold firm in the belief that market will eventually revert to fundamental anchors

• Or recognise that momentum when accompanied with EPS upgrades combined with sound valuation fundamentals offers the best of both worlds

8. Portfolio Impact: A Test of Conviction and Patience

Our portfolio’s positioning over the past 18 months reflects this tension:

• An underweight to financials, most notably CBA, and

• An overweight to healthcare, notably CSL.

This has materially weighed on performance. Over the last 12 months we have watched the P/E valuation of CBA accelerate past CSL, despite the latter poised to deliver superior earnings growth over FY25-FY27.

This divergence tests both patience and conviction. But if history is any guide, we resolutely believe the pendulum of extended extremes of high & low valuations will rebalance in time, particularly when the undervalued represent such high calibre companies.

These outcomes have informed the recent changes outlined earlier, as we recalibrate sector exposures while maintaining our long-term discipline.

As markets continue to favour momentum over fundamentals, our focus remains unchanged: to own high-quality, attractively priced businesses with enduring competitive advantages. We are confident that in time, valuation and fundamentals will reassert themselves — and when they do, portfolios anchored in discipline will be well placed.

Comments